Jet Cuts Out the Middleman

Estimated Read Time: 11 minutes

01-03-2022

Jet Insurance Company was created to provide individuals and businesses with an option to purchase surety and fidelity bonds directly from the issuing carrier. Currently, the market is dominated by agents and brokers who steer the applicant to their favored insurance company, not necessarily the company that is best for the customer. Oftentimes, surety bond buyers never interact with the carrier who is setting rates, handling claims, and making the ultimate decisions on the bond.

Ever Hear the Joke About the Surety Broker on Welfare?

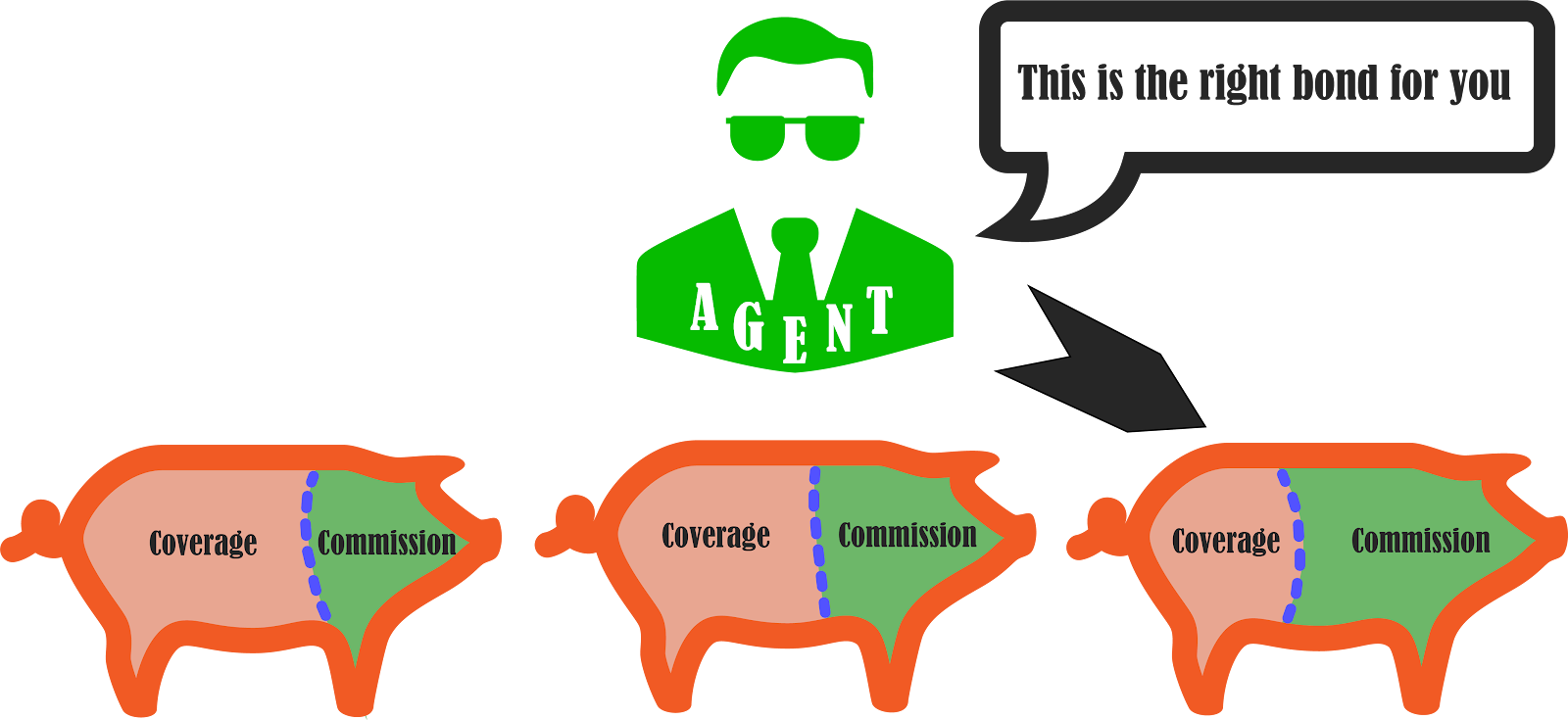

Neither have we. The single largest benefit of cutting out the middleman is removing the massive commissions paid to agents and brokers. Surety brokers are commonly paid commission rates upwards of 40% of the premium you pay. You heard that right! Almost half, and in some cases more than half, of the money you pay to purchase a surety bond goes to a middleman with no skin in the game.

We’re not suggesting agents cannot add value to the insurance buying process, but 40%??!! Also, let’s consider the nature of a surety bond. Unlike many forms of insurance, surety bonds are drafted by the Obligee, the entity requiring the bond, so there is usually no differentiation in the protection offered in the legal contract. Insurance policies are drafted by the carrier and protect the buyer of the policy so agents can assist their customers in understanding the coverage offered and tailoring a policy, or sometimes a collection of policies from various carriers, to suit their needs. Surety bonds are required, typically by government entities issuing a license, contract, or waiver, so there is much less value for an agent to provide.

Jet uses the savings from not paying agents and brokers to reduce premiums charged to customers and to invest in technology, which we believe will enable greater services and efficiencies, allowing Jet to further reduce premiums. To be fair, Jet must replace the marketing and customer service functions currently handled by brokers, which are expensive to be sure, but 40% of the premium sounds more than a little excessive to us.

Takeaway: if you want to avoid paying a surety bond premium inflated by high commissions paid to agents and brokers, cut out the middleman and buy direct from Jet.

How Many Ways Can an Insurance Broker Make Money?

Unfortunately for buyers of surety bonds, a lot. When you cut out the middleman, you’re not just cutting out the heavy commissions embedded in your premium; you’re also eliminating the potential for a host of fees to be added to your bill.

The largest and most common fee charged by middlemen is the “broker fee”. As the name implies, this fee is charged for brokering, i.e. acting in the capacity of an intermediary or “middleman”, the bond on your behalf.

According to Merriam-Webster, a broker in the insurance context is an agent who negotiates contracts. Most insurance contracts aren’t negotiated — the insurance carrier writes the contract and the prospective insured buys the policy or does not. At least with insurance policies, the agent can help the client understand the strengths and weaknesses of the various policies offered for the type of insurance needed and select the right policy to manage the unique risks of the customer.

While there are thousands of different surety bonds, you only need one specific bond to satisfy a given requirement, and the carriers who offer it all use the same bond form. Surety brokers simply need to help you identify the correct form (not for nothing, but we think the 40% commission more than covers that effort). Surety agents and brokers typically justify broker fees because they’re shopping the rate on your behalf. So you pay them to find you a lower price, one that is hopefully low enough to offset their added fees. Get all that?

We’d rather just give you a low price that isn’t stuffed with a big commission. The only way to sustainably lower the price of an identical product like a surety bond is to reduce expenses, and agents’ commissions represent the single largest expense in the surety bond process.

Broker fees aren’t the only fees charged by insurance agents and brokers on surety bonds. Need to cancel your bond? There’s a fee for that. Want to reinstate your bond after canceling? There’s a fee for that too. Need your bond shipped to you right away? You guessed it - more fees.

Carriers like Jet must justify to regulators any fees charged to customers in an arduous process known as a rate filing. All carriers must do this, but Jet is unique in that it sells surety bonds directly to the customer of the bond so you are guaranteed to only pay what’s in Jet’s rate filing because you interact directly with us. Agents and brokers are much less regulated, especially when selling insurance to businesses as in most surety bond transactions, and can often tack on fees with simple disclosures.

Takeaway: if you want to avoid the myriad fees charged by brokers, cut out the middleman and buy direct from Jet.

Planes, Trains, and Automobiles

In addition to the money absorbed by agents and brokers, the presence of a middleman creates substantial delays and extra work in the process of obtaining a bond. First, the agent or broker must collect your information and decide which insurance company has the appetite for the bond and your business or personal profile. Depending on the carrier, the agent or broker may need you to complete, sign, scan, and send a special application for that carrier. Then the agent will have to wait for the carrier to (hopefully) approve and provide a premium rate. After the agent collects your premium (and fees), the middleman must go back to the carrier to issue the bond. If you’re in the market for a court bond, a performance bond, or a fidelity crime bond, just to name a few, expect the process to take days or even weeks with middlemen involved.

At Jet, all bonds are quoted, billed, and issued automatically online. Also, Jet conducts a tremendous amount of research before offering a bond, making the process as smooth and streamlined as possible, so you can bet that Jet’s offer will save you time and money. Finally, Jet is the only carrier to offer monthly payment options on surety bonds. If you’re working with an agent and don’t want to pay for a year or more upfront, you’ll need to involve a premium finance company (yet another middleman) that brings along more applications and high interest rates.

Of course, obtaining a copy of the bond is not the ultimate goal; the bond must be filed with the entity that required you to obtain it in the first place. Most agents and brokers simply mail you a copy of the original bond, which is hopefully signed and sealed properly, leaving you to figure out how the bond is filed with the Obligee. Because Jet is an insurance carrier authorized to issue these bonds, the Obligee will often work with us on a more efficient filing process so Jet can file the bond for you.

Takeaway: if your time is money, cut out the middleman and bond with Jet.

Does the Choice of Surety Carrier Matter?

We think so. Surety agents and brokers will likely place your bond with the insurance carrier that pays them the highest commission rate. Agents and brokers negotiate agreements with carriers, in which commission rates range from 20-50%, a huge difference in profitability for the agent. Carriers generally pay higher commission rates to agents and brokers that promise and deliver higher premium volume. This means that not only is your agent or broker motivated by the commission rate instead of just making you happy, but they might “need” to place you with a certain carrier to meet volume commitments, irrespective of what that might mean for you.

Alright, so that’s how the surety bond sausage gets made, but does anyone get hurt? We think you could. Not only should your agent place your interests ahead of their commission rate out of principle, but there are key differences between the carriers, which should be the brokers’ focus.

Key carrier practices:

- Claims handling

- Refunds

- Commitment to the line of business

Claims Handling

Surety claims are different from insurance. The surety company is responsible for determining whether the claim is valid and if so must compensate the claimant unless you, the bond principal, does so first. If the surety company pays the claim it has the right to recover all amounts paid, including its claims handling and defense expenses, from you.

Often, the surety company can notify a licensing or other authority of an unreimbursed surety claim creating a mark on your record and potentially a suspension of your business license or other ramifications depending on the bond and the jurisdiction. Therefore, you want a surety who will diligently investigate your claim to determine its validity and work with you to quickly resolve it in the event the claim is deemed valid. Investigations are expensive so some insurance companies find it more profitable to simply pay claims and seek reimbursement, potentially costing you money, damaging your reputation, and creating regulatory headaches.

Jet’s mission is to do everything in its power to make the surety bond process easy. From ensuring you’re purchasing the right bond all the way to handling a claim (should it ever come to that), Jet works hard so you can spend your time and money growing your business.

Refunds

As with insurance policies, most surety bond premiums you pay are supposed to be earned by the insurance carrier over the term of the bond. This means that if you purchase a one-year term, the surety bond insurance company only earns 1/365th (~0.3%) per day. The rest is required to be placed in an “unearned premium reserve” from which the insurance company must pay you back should the bond be canceled for any reason. There are a few exceptions, such as when a bond is canceled due to a claim, where a carrier may legitimately hold unearned premium as collateral against the claim.

However, many carriers include “minimum earned premium” in the rates they must get approved by regulators, which typically range from $100-250. Some carriers go so far as stipulating the entire first year of the premium will be treated as “fully earned”. This means that even if you cancel your bond after the first day, you only get amounts paid in excess of the minimum or nothing at all. Many license and permit bonds only cost $100 so you could risk all of your premium if you found out you no longer need the bond shortly after purchasing. The industry justifies these minimum earned premiums, which are buried deep in arcane regulatory filings and almost never disclosed by brokers when you buy the bond, by saying that there is a minimum expense to issue the bond. We find that justification lacking. The broker is also required to give his or her commission, the highest expense associated with a surety bond, back on the unearned portion of the premium (more on that below).

Jet does not file minimum earned premiums. If you cancel the bond, you get your money back. As for the expense, which is very real for a company like Jet that isn’t paying agents commissions to handle these processes for us, we think it’s our job to invest in automation and other efficiencies so that we can provide you the flexibility to cancel your bond without fear of getting stiffed on your refund.

Commitment to the Line of Business

Another major differentiator among surety bond insurance carriers is their level of commitment to offering surety bonds long term. For most carriers, surety is a relatively small line of business that gets cut during bad economic cycles when surety bond claims losses spike and during other corporate restructurings. For traditional insurance companies, surety is often “last-in-line” to receive funding for technology that improves the customer experience, so even though most insurance today is done online, some surety carriers still operate with paper applications and even typewriters! At Jet, we invest heavily in our customers’ experience as evidenced by custom technology that makes the surety bond purchase quick and easy.

We’ve seen insurance carriers who are exiting a line of surety cancel all of their customers’ bonds before their scheduled renewal date causing major headaches, and even licensing and other major business problems for their clients. Even if the carrier handles its exit more responsibly, losing surety credit can be devastating for businesses that rely on it and have spent years building their reputation with a surety company.

Surety is Jet’s only line of business. Our commitment to providing you surety bond services is absolute.

Takeaway: if you want a surety partner committed to your business, cut out the middleman and bond with Jet.

Wait! There’s Still More Fine Print?

Sadly, yes. In addition to commissions, fees, delays, and conflicts of interest, agents and brokers add language to agreements they require you to sign to obtain the bond that is (yep, you guessed it) good for them and bad for you. One common example worth noting is a provision that all premiums are fully earned when the bond is issued. Even though the surety carrier is required to return any unearned premium, subject to any minimum earned premiums approved by the regulators, most agents and brokers simply attempt to override that in indemnity agreements or broker agreements. No matter how legitimate your reason for cancelation — and even though the department of insurance requires the insurance carrier to return the money — the middleman inserts language into a side agreement with you nullifying your right to the refund while protecting their right to retain their commission.

One of the reasons middlemen often get away with this is because they are very lightly regulated relative to an actual insurance company like Jet. Agents and brokers are technically overseen by state departments of insurance, but they do not face regular examinations, which are very probing on the underwriting, billing, and claims practices of insurance carriers. If you file a complaint with your state department of insurance, the broker will probably back down and return your premium, but who needs that?

Takeaway: if you want to avoid hidden fees & penalties, cut out the middleman and bond with Jet.

By cutting out the middleman, Jet Insurance Company can sustainably reduce premiums by removing the hefty commissions paid to agents and brokers, eliminating broker and other fees charged by middlemen, and removing the delays and bottlenecks created by inserting multiple parties into what should be a simple transaction. Jet’s products and services are designed with you in mind, 100% of the time.

Written by Spencer Siino, CEO of Jet Insurance Company